Behind on Payments? Your Real Options in New Jersey After the 2025 Market Reset

Behind on Payments? How the 2025 Housing Market Reset Affects New Jersey Homeowners Under Pressure

By Robert "Bob" Millaway, AI Certified Agent™ & South Jersey Lifestyle Specialist

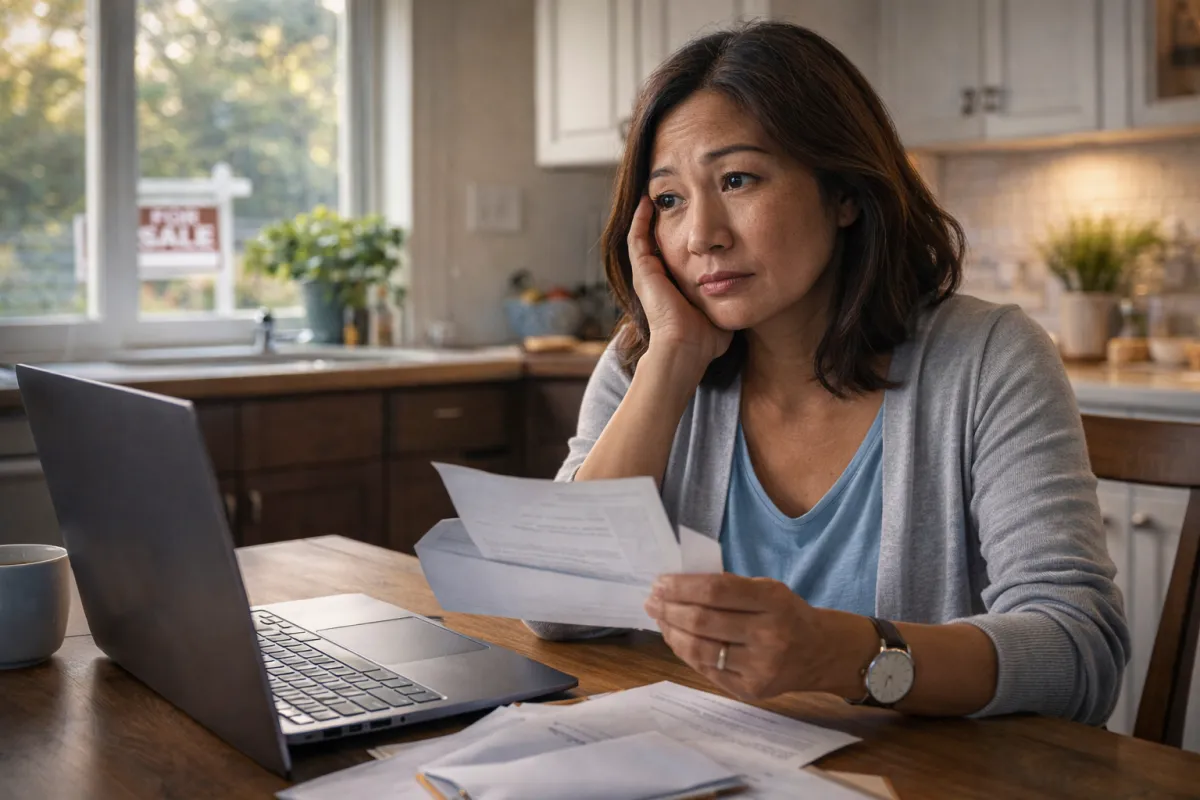

If you're behind on mortgage payments , or worried you might be soon , it's easy to assume the housing market is working against you.

But according to national data, the 2025 housing market didn't collapse. It reset. Prices flattened, inventory increased, and the market returned to fundamentals instead of frenzy.

For New Jersey homeowners under financial pressure, that reset has created more clarity , and often more options , than the headlines suggest. As 2026 begins, this reset has already changed how buyers, lenders, and homeowners interact , especially for those under financial pressure.

Read more about the 2025 Housing Market Reset: What New Jersey Homeowners Need to Know

This Is Not a Repeat of the 2008 Housing Crisis

One of the biggest fears distressed homeowners have is that values will suddenly disappear.

The data shows that's not what's happening.

National home prices finished 2025 essentially flat, remaining well above pre-pandemic levels. Inventory rose, but forced selling remained limited, particularly in the Northeast.

In New Jersey, that matters because:

New construction remains constrained

Many homeowners still hold meaningful equity

Demand hasn't vanished , it's become selective

Recent data from key New Jersey markets shows median home prices declined 3.1% year-over-year in towns like Freehold, Ridgewood, and Princeton, but this represents market normalization rather than collapse. Home values remain approximately 80% above pre-COVID levels.

This is a market adjusting to reality, not unraveling.

Why a "Normalizing" Market Can Help Homeowners in Distress

As inventory returned in 2025, sellers were forced to engage in price discovery , adjusting expectations to match real buyer demand.

Price reductions became more common nationwide, not as a sign of distress, but as evidence that the market was functioning again. In New Jersey, inventory surged 7.2% in key markets, while the sale-to-list ratio stands at 101.2%, meaning homes still sell close to asking prices.

For homeowners under pressure, this shift matters because:

Buyers are still transacting at realistic price levels

Certainty now carries more weight than peak pricing

Liquidity exists for sellers willing to engage the market

In practical terms, you don't need perfect conditions to sell , you need workable ones. While homes are sitting on the market 10% longer than last year, they're still selling when priced correctly.

When Waiting Reduces Options Instead of Preserving Them

Many homeowners delay action because they hope conditions improve.

But in a fundamentals-driven market, waiting can quietly reduce leverage.

If you're dealing with:

Missed or late mortgage payments

Mounting credit card or medical debt

Divorce, probate, or loss of income

Lender notices or legal letters

The earlier you explore options, the more control you keep over the outcome.

The market now rewards execution , not hesitation. With average days on market increasing, homeowners who wait for perfect conditions may find themselves competing with more inventory while dealing with mounting financial pressure.

Selling Is One Option , But Not the Only One

It's important to say this clearly: selling is not always the right move.

Some homeowners benefit from:

Loan modifications , Permanent changes to loan terms

Repayment plans , Structured catch-up arrangements

Temporary forbearance , Pause or reduction in payments

Staying put while stabilizing finances

But for others, selling , especially without repairs, showings, or long timelines , provides clarity and relief.

The key is understanding your actual position in today's market, not guessing based on outdated assumptions. With New Jersey's median list prices at $563,048 against a median household income of $96,278, the affordability gap creates ongoing challenges that require realistic assessment.

Why Certainty Matters More Than Ever for Distressed Sellers

The 2025 market reset highlighted something many homeowners overlook: certainty has real value.

Traditional listings can still work , but they require:

Time (homes now average longer market time)

Repairs and staging

Multiple showings

Buyer financing approval

Uncertain timelines

For homeowners under pressure, uncertainty can be costly.

That's why some New Jersey homeowners choose a direct, as-is sale , not because it's a last resort, but because it offers:

A defined timeline

No repairs or clean-outs

No commissions

A clear outcome

It's not about maximizing price at all costs. It's about solving the problem without creating a new one.

Consider exploring options at robertmillaway.com/sell/sell-my-home if you need a straightforward assessment of your situation.

A Calm Next Step: Get Clear on Your Options

If financial pressure is part of your situation, the most important step isn't making a decision , it's getting accurate information.

A simple, no-obligation conversation can help you understand:

What your home is realistically worth today

Whether selling makes sense in your situation

What a clean exit could look like if needed

There's no commitment, no pressure, and no judgment , just clarity.

Whether you choose to list traditionally, sell directly, or do nothing at all, knowing your options restores leverage. You can schedule a consultation at robertmillaway.com/schedule-call to discuss your specific circumstances.

For homeowners exploring traditional selling after the market reset, check out our guide on Selling a Home in New Jersey After the Market Reset.

The AI Advantage in Today's Market

As an AI Certified Agent™, I use advanced market analysis tools to provide homeowners with real-time insights about their property value and selling options. Our AI Listing Advantage program helps distressed homeowners understand their position quickly and accurately, removing guesswork from critical decisions.

This technology is especially valuable for homeowners under pressure who need precise information fast. Learn more about our innovative approach at robertmillaway.com/sell/ai-marketing-strategy.

Final Thoughts

The 2025 housing market reset didn't create a crisis , it created clarity. For New Jersey homeowners behind on payments or facing financial pressure, this normalized market offers more predictable outcomes and multiple pathways forward.

Whether you pursue loan modifications, forbearance, traditional selling, or direct sale options, the key is acting from a position of knowledge rather than fear. The market is functional, buyers are active, and solutions exist for homeowners willing to engage realistically with current conditions.

Your situation is unique, and the right strategy depends on your specific circumstances, timeline, and goals. But understanding your options , all of them , is the first step toward regaining control.

FAQ

Q: Will home prices continue to fall in New Jersey?

A: The 2025 data shows price stabilization rather than continuous decline. While some markets saw 3.1% year-over-year decreases, values remain well above pre-pandemic levels. Future price movements depend on local inventory and demand dynamics.

Q: How long does it take to sell a home in New Jersey's current market?

A: Homes are taking about 10% longer to sell compared to 2024, but well-priced properties still move within reasonable timeframes. The key is realistic pricing and condition.

Q: What if I owe more than my home is worth?

A: Even if you're underwater on your mortgage, you may have options including loan modifications, short sales, or deed-in-lieu arrangements. Each situation requires individual assessment.

Q: Should I wait for the market to improve before selling?

A: Waiting can reduce options for homeowners under financial pressure. Current market conditions provide liquidity for motivated sellers, and delay often increases carrying costs and stress.

Q: What's the difference between forbearance and loan modification?

A: Forbearance temporarily pauses or reduces payments but doesn't change loan terms permanently. Loan modification permanently alters your loan structure, potentially reducing payments long-term.

Q: Can I sell my home if I'm behind on payments?

A: Yes, you can typically sell even if you're behind on payments, though the process may require coordination with your lender. The proceeds would pay off the mortgage balance and any arrears.